For some time now, blockchain has been revolutionizing the way we see banking, fintech, digital identity, supply chain management and even the healthcare system. An IBM study which surveyed more than three thousand executives has revealed that at least 80% of respondents are actively using or planning to integrate blockchain technology into their businesses.

Although there still are a lot of companies that continue to rely on traditional, central databases to generate revenue, this technology has gained considerable ground in the last 3-5 years. Moreover, according to Gartner, blockchain is expected to generate an annual business value of more than USD 3 trillion by 2030. The same report shows that 82% of reported blockchain use cases were registered in the financial sector in 2017, yet, the percentage dropped to 46% in 2018.

Nevertheless, more recent statistics indicate that financial services are still considered to be the current and near-term future leader of blockchain, with high potential also seen in industrial products, energy and utilities as well as healthcare.

What is blockchain?

Blockchain has made its public debut in 2008 when Satoshi Nakamoto, whose real identity is still under discussion, released the whitepaper Bitcoin: A Peer to Peer Electronic Cash System. However, the first work on a cryptographically secured chain of blocks was described in 1991 by Stuart Haber and W. Scott Stornetta, two researchers who wanted to implement a system where document timestamps could not be tampered with.

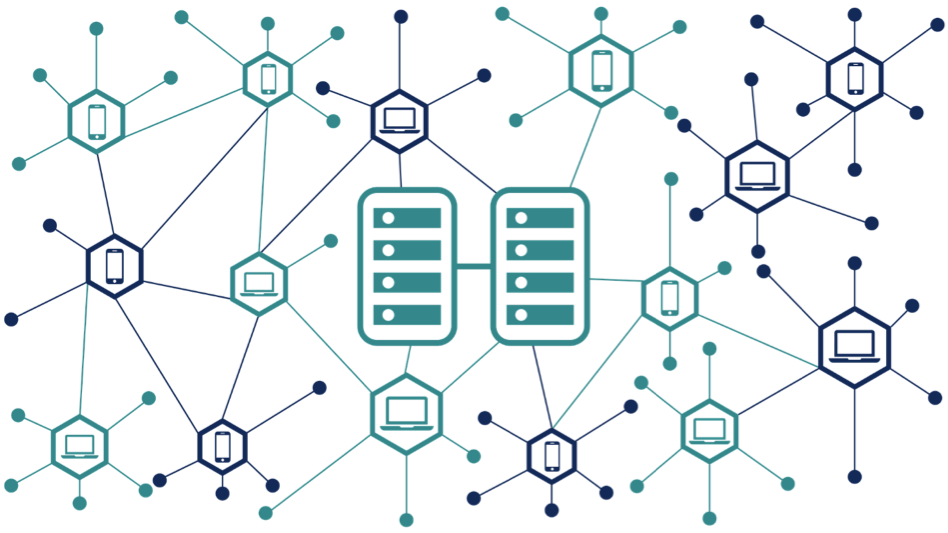

Blockchain is a distributed and public ledger used to record transactions across many computers. Simply put, it is a decentralized saving data structure. The details of the transactions cannot be altered retroactively, without tampering all subsequent records, which actually makes the modification of data really difficult. Even though this is not exactly impossible, so far blockchain has proved to be more secure than other technologies.

Some researchers consider that the way blockchain is used is similar to the internet and that is why they have called it “the internet 3.0”. The technology can be used to develop blockchain applications, including social networks, messengers, games, exchanges, storage platforms, voting systems, prediction markets, online shops and many other.

Main characteristics of the blockchain technology

A blockchain network has a series of characteristics that make it so popular among business owners.

- Decentralized – it is not owned or controlled by a single entity. Each of the blocks of data is secured and bound to each other using cryptographic principles. All parties involved have a copy of the ledger;

- Immutable – even though everyone has access to the ledger, no one can tamper with the data that is inside the blockchain;

- Enhanced security – apart from not being a centralized system, the use of cryptography is another thing that adds an extra protection layer. Every information on the blockchain is hashed cryptographically, which means the information on the network hides the true nature of the data. For this process, any input data gets through a mathematical algorithm that produces a different kind of value, but the length is always fixed;

- Anonymity – since blockchain transactions are represented as a sequence of numbers, nobody can tell who they belong to;

- Consensus – a transaction is accepted and recorded on the blockchain as long as all the participants agree to follow the same rules. A transaction will be considered invalid if it violates one of the rules the network agreed upon.

4 aspects businesses should reflect on before adopting blockchain

The blockchain is clearly a great innovation and companies are really hyped about using this technology to enhance their businesses. Blockchain can be used to improve efficiency, secure processes and cut costs by removing unnecessary middlemen. But there are certain aspects that should be considered before jumping in the blockchain bandwagon.

Firstly, before investing in blockchain technology, companies should perform a strategic evaluation of their business model and business needs to see if this is really a good fit. If your company has dependencies on a third-party that sometimes is more of a hassle, blockchain might really help. Of course, this will also depend on the business type and on the area where it is to be implemented.

Yet, in some cases, the challenges a company faces can be solved in other ways that do not involve blockchain, including by reworking several legacy-based solutions.

Secondly, once a decision to go with blockchain has been made, companies need to prepare and follow a strategy that will allow them to leverage the maximum benefits of blockchain technology. Defining a strategy also includes deciding whether to use a public blockchain (where anyone can join and be a part of the network) or a permissioned blockchain (where all those who want to become part of the network must be assessed by the current participants). If your company is not quite ready to handle large amounts of transactions and data, then a permissioned blockchain might be the best approach.

Thirdly, the cost is a significant aspect that has a great impact during the decision-making process. Mainframe, storage and energy costs are the top three things that need to be considered. Energy costs may rise substantially as the transaction volume increases.

Lastly, the effect these changes will have on employees and customers is also an important factor. According to a Juniper Research survey, 35% of companies think that blockchain integration will cause disruption to their internal operations, while 51% feel it will cause a “significant disruption” to their partners and customers. Just think about Bitcoin and the impact it had on people and on the Fintech industry.

Needless to say, blockchain technology has the potential to reshape the existing models. Companies that want to integrate it into their operations need to understand how it works and, more importantly, if it really works for their company.

If you’re a business owner looking to know more about blockchain and whether or not to implement it into your company, get in touch with us and we can help you see how it can benefit your business. We at Expert Network believe that, with the right guidance and the proper tools, any idea can be turned into a successful solution. Your vision, coupled with our extensive knowledge in business areas such as automotive, HORECA, retail & services, all supported by a revolutionary technology such as blockchain, can be the key towards a powerful product.